Synopsis: The government has cleared a massive oil bond hangover, money borrowed two decades ago to keep petrol cheap. The debt is gone. But the savings may not reach your tank. Let’s dive into the specifics.

Picture this. You have been paying monthly instalments on a credit card that you did not swipe. Someone else charged in your name, years before you even knew about it. That, in simple terms, is what India has been doing with oil bonds since 2005.

This March and April, the Indian government finally cleared the last tranche of ₹1.53 lakh crore in oil bonds. Add in almost two decades of interest, and the total bill reaches ₹3.23 lakh crore. That is one of the largest hidden-debt cleanups in independent India’s fiscal history.

So the natural question follows: now that the debt is gone, will petrol and diesel get cheaper? The short answer is not automatically. Here is why. What were these oil bonds, exactly?

Go back to 2004. Crude oil was around $40 a barrel. Within four years, it hit $144. For India which imports roughly 85% of its crude that was a body blow.

Source: Tradingview

The three state oil companies, IOC, BPCL, and HPCL, were caught in a trap. They had to buy expensive crude on global markets. However, the government told them to sell petrol and diesel cheaply at home. The gap between cost and selling price is called an under-recovery. It was bleeding them dry.

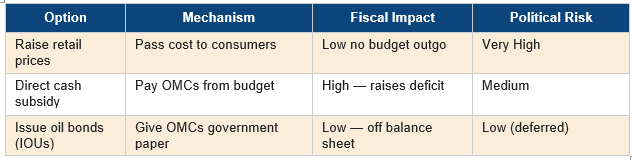

The UPA government faced a real dilemma. Raising fuel prices would push up inflation and anger voters. Paying cash to the oil companies would blow up the fiscal deficit. So it chose a third option: give the companies government bonds essentially IOUs instead of cash.

The clever part? These bonds did not show up as direct spending in the Union Budget. The fiscal deficit looked healthier than it was. Economists call this off-balance-sheet financing. Critics call it financial sleight of hand. “The true cost of subsidising fuel was not eliminated. It was hidden and paid later, slowly, invisibly, with compound interest added on top.”

How the UPA government chose to handle the fuel crisis:

How the debt ballooned and who repaid it

When the NDA government came to power in 2014, it inherited these bonds as a non-negotiable obligation. The principal repayments would start falling due from the early 2020s.

On the other hand, global crude prices crashed in late 2014. Brent fell from over $100 to below $30 by early 2016. Most countries passed that savings on to consumers. India did not. Instead, the Centre raised excise duties on petrol and diesel nine times between November 2014 and January 2016.

The argument was consistent: Finance Minister Nirmala Sitharaman repeatedly called the oil bonds a legacy burden from the UPA era. High fuel taxes, the government said, were needed to repay that debt.

Significant repayments happened in chunks. Around ₹10,000 crore was paid in FY2021-22. Then ₹31,150 crore went in FY2023-24. The final balance clears in March–April 2026. Then came the Ukraine shock a second wound

Just as India was managing the bond repayment cycle, Russia invaded Ukraine in February 2022. Crude surged from $80 to over $130 per barrel in under eight weeks.

History repeated itself. With state elections approaching and the 2024 general election in sight, the government froze retail fuel prices. Once again, IOC, BPCL, and HPCL absorbed losses on every litre sold.

Since then, crude has softened to the $70–80 range. The government has allowed oil companies to keep retail prices steady even as input costs fell. This price stickiness is deliberate. It quietly lets OMCs rebuild their balance sheets. The repair process might need 18–24 more months.

How Severely Have These OMCs Suffered?

1. Indian Oil Corporation (IOC)

IOC is India’s largest oil refiner and fuel retailer, controlling roughly 42% of the petroleum market. During the oil bond era, it received the largest share of government IOUs in place of cash bonds it carried on its books for nearly two decades.

When the Ukraine shock hit in 2022 and retail prices were frozen, IOC’s net profit collapsed 66% in a single year, falling from ₹24,184 crore in FY2021-22 to ₹8,242 crore in FY2022-23.

Its refining scale and diversified revenue petrochemicals, pipelines kept it from slipping into a full loss, unlike its peers. By FY2023-24, profits had recovered sharply to ₹39,618 crore, largely through the silent margin recoupment phase as crude eased and retail prices held steady.

2. Bharat Petroleum Corporation Limited (BPCL)

BPCL operates refineries in Mumbai and Kochi and runs one of India’s widest fuel retail networks. The Ukraine crisis hit it unevenly two consecutive loss-making quarters in FY2022-23, followed by a strong recovery in Q4. The full-year net profit for FY2022-23 came in at just ₹2,131 crore, down 81% from ₹11,682 crore the previous year.

The oil bond clearance matters for BPCL beyond just balance sheet optics the company has been a recurring privatisation candidate, and potential buyers had long flagged the bond-related uncertainty as a concern. A cleaner balance sheet now makes it a more straightforward acquisition target, if the government revives that process.

3. Hindustan Petroleum Corporation Limited (HPCL)

Of the three, HPCL took the hardest blow. It posted a standalone net loss of ₹8,974 crore in FY2022-23 with ₹10,197 crore of that lost in Q1 alone, when crude was above $120 and retail prices were frozen. Debt jumped 45% in a single year, from ₹48,498 crore to ₹70,671 crore, as the company borrowed to fund crude it was selling below cost.

Despite the recovery, its debt remains elevated, making it the most financially vulnerable of the three to any future government-mandated price cut.

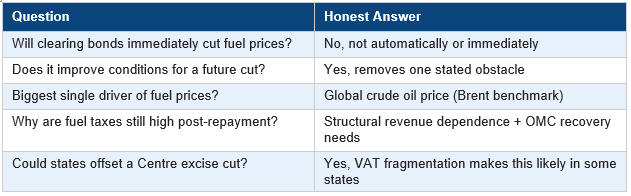

So will fuel prices actually fall?

The oil bond repayment does improve things. The ₹9,000–10,000 crore annual interest drag disappears. The government no longer has its go-to justification for keeping excise duties high. OMCs have cleaner balance sheets. India’s fiscal standing with global rating agencies also gets a modest boost.

However, clearing the bonds does not automatically mean cheaper fuel. There are five big reasons why.

- Excise is now a revenue pillar, not a debt tool. Petroleum taxes raise roughly ₹5–6 lakh crore per year. The saved interest of ₹10,000 crore is less than 0.2% of that total.

- Global crude is the dominant variable. If Brent rises due to OPEC+ cuts or Middle East tensions, any excise reduction gets wiped out quickly.

- OMCs are still recovering. A forced price cut before balance sheet recovery is complete would reopen FY2022-23 wounds. The government won’t recapitalise them through the budget.

- State VAT complicates everything. VAT rates range from 15% to 36% across states. A central excise cut shrinks the VAT base, so some states simply raise their rates in response.

- Electoral timing matters. Fuel price cuts cluster before major elections. The next general election is not due until 2029 political urgency is low right now.

Think of it like paying off a long-standing credit card debt. Your finances improve. You feel lighter. But you do not necessarily spend less next month you might redirect that money to rent, groceries, or savings instead.

For Indian consumers, the most realistic near-term outcome is not cheaper petrol. It is, however, a stronger political case to resist future price hikes. If crude stays low and state elections align, a modest ₹2–4 per litre excise cut on diesel which powers freight and agriculture is possible within the next two years.

The deeper legacy of the oil bond repayment is not about the pump price. It is about honesty in public finance. The cost of subsidising fuel in the 2000s was never eliminated. It was deferred, hidden, and passed on to future taxpayers with two decades of compound interest quietly added on top. That bill, at least, is now paid.

Disclaimer: The views and investment tips expressed by investment experts/broking houses/rating agencies on tradebrains.in are their own, and not that of the website or its management. Investing in equities poses a risk of financial losses. Investors must therefore exercise due caution while investing or trading in stocks. Trade Brains Technologies Private Limited or the author are not liable for any losses caused as a result of the decision based on this article. Please consult your investment advisor before investing.

{kind=link}