4 min readMumbaiUpdated: Aug 1, 2024 05:30 AM IST

An Unfavourable base effect brought down the overall non-food credit growth of the banks to 13.9 per cent at Rs 163.46 lakh crore as of June 30, 2024 as against 16.3 per cent in June 2023, even as gold and housing loans rose sharply, according to the Reserve Bank’s latest data.

The growth in credit card outstanding, meanwhile, declined during the 12-month period.

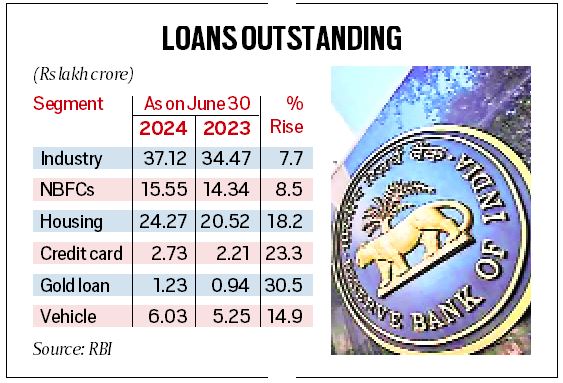

Analysts have attributed the slower rate to RBI measures such as higher risk weights on unsecured loans, a higher base effect and banks’ focus on managing the credit-to-deposit ratio. Gold loan outstanding jumped by 30.5 per cent to Rs 123,776 crore as of June 2024 from Rs 94,872 crore (19.3 per cent growth) in June 2023. Credit card outstanding rose by Rs 51,000 crore to Rs 273,044 crore, showing a slower growth of 23.3 per cent as against 37.6 per cent a year ago, according to RBI data.

“The rise in gold loans could be due to the sharp rise in gold prices in the last one year which prompted people to pledge gold to raise finances,” said a banking source. Gold loan NBFCs also hold a sizeable gold portfolio with Muthoot Finance alone accounting for a loan asset portfolio of Rs 63,200 crore in 2023.

Overall growth in the personal loan segment was lower at 16.6 per cent (Rs 50.91 lakh crore) in June 2024 as compared to 21.3 per cent a year ago, largely due to moderation in growth recorded in ‘other personal loans’ and ‘advances against fixed deposits’. However, credit growth to housing, the largest constituent of the segment, accelerated by 18.2 per cent at Rs 24.27 lakh crore in June 2024 from 14.8 per cent (Rs 20.52 lakh crore) a year ago, RBI data shows.

RBI measures to check the unprecedented growth in unsecured loans had slowed down the growth in the segment. In November 2023, the RBI had increased risk weight on the exposure of banks towards consumer credit, credit card receivables and non-banking finance companies (NBFCs) by 25 per cent up to 150 per cent. The move was aimed to address build-up of any risks in these segments.

RBI data shows that credit growth to agriculture and allied activities remained robust at 17.4 per cent (y-o-y) in June 2024, but it was lower compared with 19.7 per cent a year ago.

Story continues below this ad

Credit to industry grew at 7.7 per cent to Rs 37.12 lakh crore in June 2024 as compared with 7.4 per cent in June 2023. Among major industries, while y-o-y growth in credit to chemicals and chemical products, food processing and infrastructure was higher in June 2024, credit growth to basic metal and metal product, petroleum, coal products and nuclear fuels and textiles moderated, RBI says.

However, credit growth to services sector moderated substantially to 15.1 per cent in June 2024 from 26.8 per cent a year ago, primarily driven down by lower credit growth in non-banking financial companies (NBFCs) and trade segments.

According to CareEdge Ratings, if the credit and deposit inflows over the past 3 months and 6 months are studied, credit offtake at 5.3 per cent for six months and 2.3 per cent for 3 months has lagged the deposit growth numbers of 6.0 per cent and 3.4 per cent for a similar period.

Meanwhile, in absolute terms, deposits expanded by Rs. 23.9 lakh crore over the last 12 months and reached Rs. 211.8 lakh crore as of July 12, 2024. Deposit growth is expected to be prominent in FY25 as banks intensify efforts to strengthen their liability franchise. The banks are also sourcing funds via certificates of deposits (at a relatively higher cost) which have shown significant traction. This aims to prevent constraints on credit uptake due to deposit growth. The absolute growth in credit offtake stood at Rs 8.4 lakh crore for six months and Rs 3.8 lakh crore for 3 months has lagged the deposit numbers of Rs 11.9 lakh crore and Rs 7 lakh crore for the similar period, CareEdge said.

© The Indian Express Pvt Ltd

{kind=link}