What do you do with a company that has near-perfect operating metrics but a stock that’s down 47% from its highs?

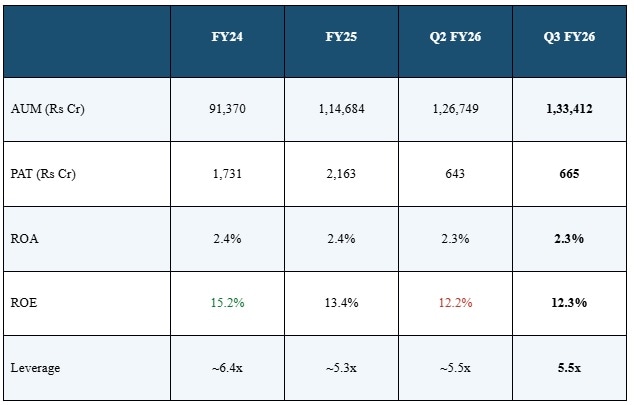

Bajaj Housing Finance went from zero to Rs 1 lakh crore in Assets Under Management (AUM) in just eight years. Gross Non-Performing Assets (GNPA) have never crossed 0.35%. The company also holds the highest domestic credit rating (AAA), and in Q3 FY26, it reported Profit After Tax (PAT) of Rs 665 crore, growing 21% year-on-year.

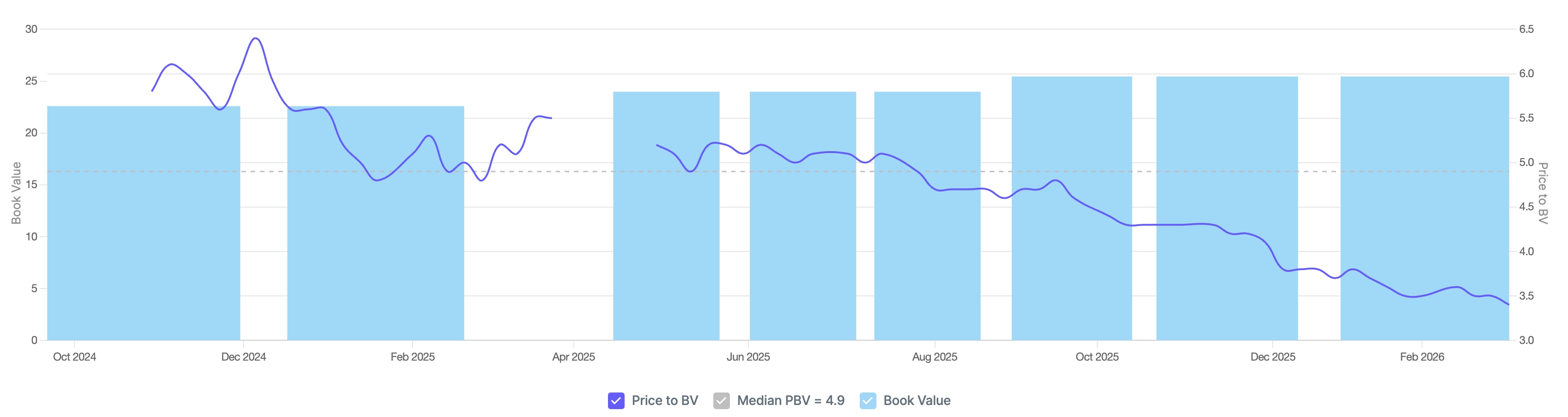

And yet, the stock is trading near its all-time low at roughly Rs 88 per share, at about 3.5x book value.

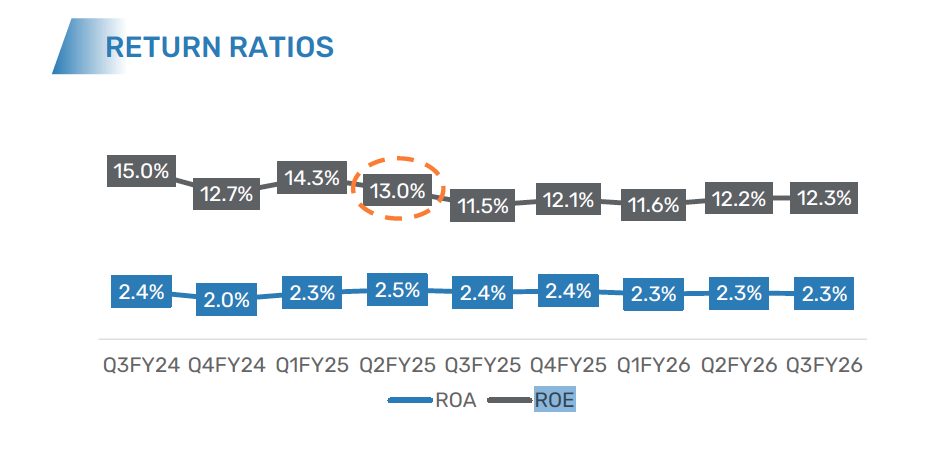

Underneath the excellent operating metrics, Bajaj Housing Finance faces a few challenges. For one, Return on Equity (ROE) has been declining every year.

Second, its affordable housing shift (the Sambhav portfolio) is growing rapidly at a time when the segment as a whole is seeing higher delinquencies.

Third, a rate cut environment is pushing borrowers towards lower yields, typically to PSU banks, which have become very competitive lately.

For a stock that listed at a massive premium and touched an all-time high price-to-book (P/B) of 10x after listing barely 18 months ago, the trajectory has clearly shifted.

Story continues below this ad

Let’s dig deeper into each factor and assess whether these are genuine structural concerns or simply market narratives.

Too much capital, not enough leverage

The decline in ROE is not about poor lending or rising defaults. It’s largely arithmetic.

When Bajaj Housing Finance went public in September 2024, it raised Rs 3,560 crore of fresh equity. That capital sits on the balance sheet, earning returns, but it pushed the company’s leverage down to 5.5x. For context, the company’s internal threshold is 8.0x, and management says it will take 2-2.5 years to deploy this capital fully.

Source: Bajaj Housing Finance Investor Presentations, Annual Report FY25

Story continues below this ad

Think of it this way: the company earns roughly Rs 2,500 crore a year on a net worth of Rs 21,800 crore. So, a top-of-the-line housing finance company with 12% ROE is trading at 3.5x book. Despite its strong pedigree, the stock is still priced for a future that hasn’t arrived yet.

Source: Bajaj Housing Finance Ltd Investor Presentation Q3FY26

Source: Bajaj Housing Finance Ltd Investor Presentation Q3FY26

There are reasons to believe that ROE could improve as management deploys the remaining capital over the next 2-2.5 years; some of that improvement is visible in the quarterly ROE, which has recovered since the Q3FY25 low of 11.5%.

Running faster to stay in place: The Balance Transfer problem

Bajaj disbursed Rs 16,545 crore in Q3, a 32% jump from last year. But AUM grew only 23%. Where did the difference go? Attrition.

Story continues below this ad

Roughly 20% of the home loan book is being refinanced every year, mostly to PSU banks offering lower interest rates. This is up sharply from 15-16% a year ago.

The management calls it a feature of the competitive landscape, not a novelty.

Balance transfers in (customers coming from other lenders) are running at 16.5% of new acquisitions, but only 40% of customers attempting to transfer are being retained. So, while the company is bringing in new customers from other lenders too, it isn’t enough to offset the outflow.

This is a structural challenge even the top private housing finance lender faces in a falling-rate environment. A lender originates a high-quality loan and seasons it for 2-3 years. Then a PSU bank poaches your de-risked customer with a rate 50 basis points lower.

The spread squeeze

Story continues below this ad

Source: Bajaj Housing Finance Investor Presentations, Q3 FY25 to Q3 FY26

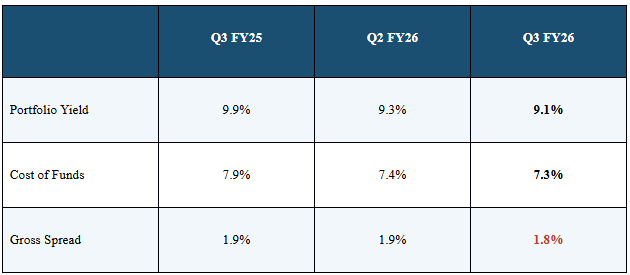

Yields are falling faster than funding costs. Over the last year, portfolio yield has declined 80 basis points (from 9.9% to 9.1%) while the cost of funds has dropped only 60 basis points (from 7.9% to 7.3%).

The CFO expects 8-10 basis points of further Net Total Income (NTI) compression for the full year. The company has passed on 60 bps in rate cuts to borrowers on the non-repo book since March. Until the rate cycle stabilises, this squeeze will continue.

The Sambhav bet: Going where banks don’t

For seven years, Bajaj Housing Finance operated in the safest corner of mortgage lending: prime salaried customers with 750+ CIBIL scores and 84% salaried mix. Home loan portfolio yield is just 8.6%, and in this segment, PSU banks compete purely on price.

Story continues below this ad

During these seven years, the financial health of PSU banks has seen remarkable improvement, leading to higher competitive intensity in the prime home loan segment.

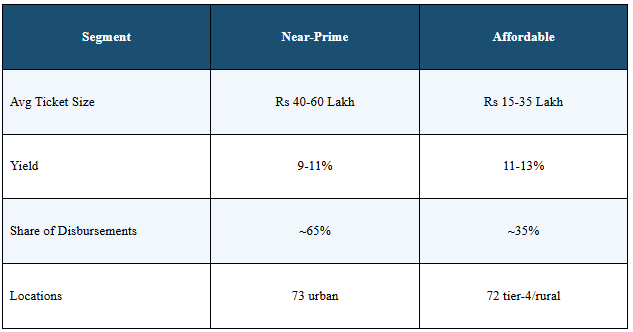

So in FY25, the company launched Sambhav, a dedicated business unit for near-prime and affordable customers. In just over a year, it has scaled to Rs 5,000+ crore in AUM and Rs 325-350 crore in monthly disbursements. The target is to double that to Rs 600+ crore a month within 12-15 months.

Source: Bajaj Housing Finance Q3 FY26 Investor Presentation and Conference Call

The yield differential is meaningful: 1.25-1.5% above the prime book. And critically, this is a segment where PSU banks are less aggressive, so the balance transfer headwind is weaker.

Story continues below this ad

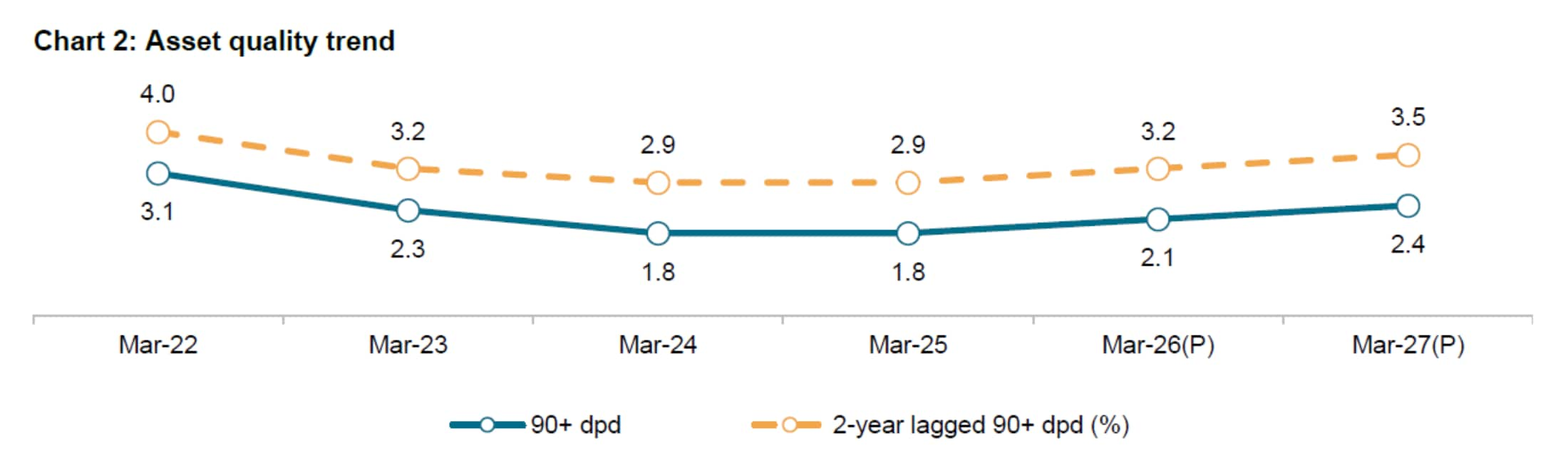

But there’s a catch. Affordable housing across the industry is showing rising stress. Between fiscal 2024 and 2025, more than 70% of A-HFCs saw a notable increase in 90+ days past due loans in the sub-Rs 15 lakh category by ~25-30 basis points. The trend continued in the first half of this fiscal year.

Source: CRISIL Press Release

BHFL’s medium-term GNPA guidance of 0.40%-0.60%, against a current 0.27%, is an implicit acknowledgement that credit costs will rise as Sambhav scales. The management insists the company is positioned at the formal, upper end of affordable and isn’t undercutting on price. But going from 86% prime to a meaningful non-prime mix is the biggest strategic bet/risk this company has made.

Given that Sambhav is only around Rs 5,000 crore against a Rs 72,769 crore home loan book (~7%), any stress there would still be invisible in the blended 0.34% home loan GNPA. That’s precisely what makes it hard to evaluate right now.

This uncertainty is further compounded by the fact that the affordable housing segment is seeing increasing delinquencies. To an untrained eye, a slight increase in GNPA might seem inconsequential, but a rising trend in GNPA at the company as well as the industry level is an omen to watch out for.

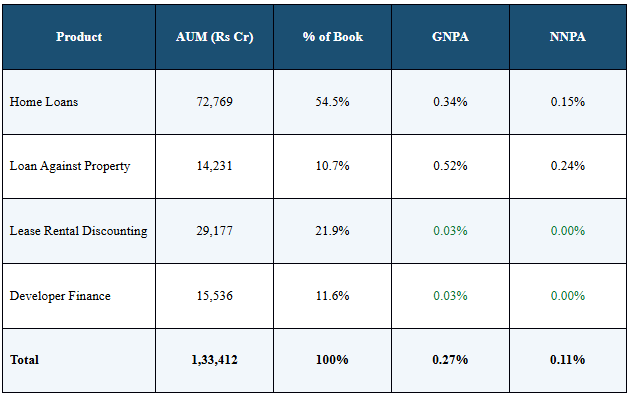

Asset quality by product

Story continues below this ad

Segment-wise GNPA is not alarming. But as previously stated, it’s the directional increase which is worrying the market.

Source: Bajaj Housing Finance Q3 FY26 Investor Presentation. Slide 34

LRD, which is 22% of the book, has had nil GNPA since inception, focusing on Grade-A commercial properties leased to REITs and MNCs. Today’s quality is exceptional. The question is where these numbers will be as Sambhav grows from Rs 5,000 crore to potentially Rs 15,000-20,000 crore.

Valuation and outlook

At Rs 88 per share and roughly 3.5x book, the stock has corrected meaningfully from post-listing highs.

But 3.5x book for a 12% ROE business is not cheap except on a relative basis, that too relative to itself a year ago. On an absolute basis, it is the most richly valued listed HFC in India.

Source: www.screener.in

Source: www.screener.in

The path to re-rating runs through three levers.

First, natural leverage. As AUM grows and equity stays fixed, leverage climbs from 5.5x toward 7-8x, mechanically boosting ROE.

Second, ‘Sambhav’. Higher-yielding near-prime and affordable loans improve the blended portfolio yield.

Third, operating leverage. The company’s opex-to-NTI ratio is 19% today against a medium-term target of 14-15% over the next 3-4 years. If all three play out, management’s medium-term ROE guidance of 13-15% is credible.

The risks are that spread compression could worsen if rate cuts accelerate, the BT-out headwind persists longer than expected, and the Sambhav push into affordable could bring higher credit costs just as the broader sector is seeing rising stress.

In conclusion, Bajaj Housing Finance is a well-run company navigating a tricky transition. The operating metrics remain strong, but the stock’s correction reflects a market realising that even the best operators need time to grow their valuations. The next 4-6 quarters will show whether Sambhav can scale without compromising quality, and whether leverage can normalise fast enough to push ROE back above 13%.

Note: We have relied on data from www.Screener.in and www.tijorifinance.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

Rahul Rao has helped conduct financial literacy programmes for over 1,50,000 investors. He has also worked at an AIF, focusing on small and mid-cap opportunities.

Disclosure: The writer or his dependents do not hold shares in the securities/stocks/bonds discussed in the article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.

{kind=link}