Over the last two years, VA Tech Wabag’s revenue grew by nearly 20% annually, its operating margin roughly doubled over a slightly longer period, it remained net cash positive, and earned a credit rating upgrade. Yet for much of that time, the stock barely moved.

The share price climbed to nearly Rs 1,940 in late 2024 before sliding to around Rs 1,034 by January 2026.

Then, in the two months following the company’s FY26 results, the stock surged about 38% to roughly Rs 1,600. Its trailing Price-to-Earnings (P/E) multiple expanded from about 19x to 27x in a matter of weeks.

So what changed? Not the business. The company had been quietly transforming itself for three years. What changed was that the market finally took notice. Three things are worth understanding here:

- The strategy reset that drove the numbers, and whether it can keep delivering.

- The receivables puzzle: how a company with Rs 3,172 crore tied up in receivables stays net cash for six straight years.

- The runway, an order book worth more than four times revenue, set against a quiet question mark over the “asset-light” model.

The reset that changed everything

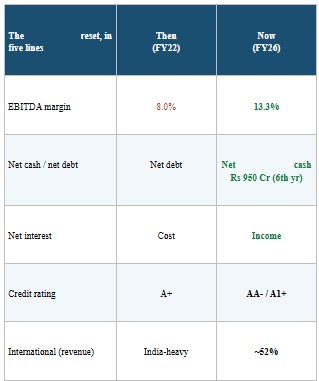

Three years ago, management laid out a medium-term plan: grow revenue 15-20% a year, hold the Earnings Before Interest, Tax, Depreciation and Amortisation (EBITDA) margin between 13% and 15%, push Return on Capital Employed (RoCE) above 20%, and remain net cash positive.

For a company whose margins had been stuck in single digits, those targets looked ambitious. Today, it has more or less delivered on all of them.

The reset had four parts, all moving in the same direction: higher margin, lighter balance sheet.

First, the company shifted from full Engineering, Procurement and Construction (EPC) work to a lighter Engineering and Procurement (EP) model, outsourcing the heavy, low-margin civil construction to third parties.

The internal mantra became “product over project, cash over revenue.” This is the single biggest reason the EBITDA margin climbed from about 8% in FY22 to over 13% today.

Strategy-led reset

Source: Company filings; India Ratings (Feb 2026); Q4 FY26 IP. Net interest cost turned to net interest income in FY26

Source: Company filings; India Ratings (Feb 2026); Q4 FY26 IP. Net interest cost turned to net interest income in FY26

Second, it tilted hard towards international work, now about half of revenue, chasing the Middle East and Africa. The reason is not glamour. Those projects are funded by sovereign governments or multilateral agencies such as the World Bank and the Japan International Cooperation Agency (JICA), which means better payment security, better margins, and faster cash collection than a typical Indian municipal contract.

VA Tech Wabag – Revenue mix

Source: VA Tech Wabag Investor Presentation – Q4FY26

Source: VA Tech Wabag Investor Presentation – Q4FY26

Third, it has been building its Operations and Maintenance (O&M) business, the part that runs plants after they are built, towards a target of 20% of revenue. O&M is already about 40% of the order book.

It is annuity income: predictable, recurring, high-margin and light on capital.

Fourth, bidding discipline. Payment security sits at the top of every bid decision, so more than 95% of the order book is backed by letters of credit, multilateral agencies or sovereigns, and the company simply walks away from risky, state-funded projects.

As management puts it, this is about value over price.

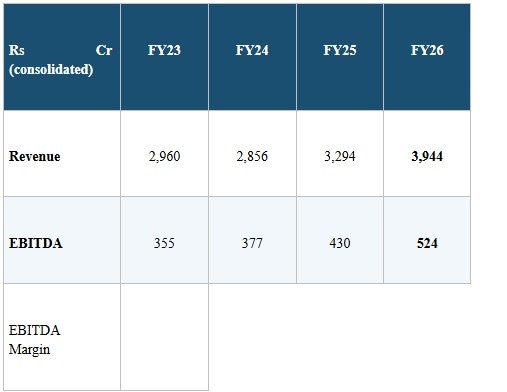

Add it up, and the financial transformation is striking.

Summarising financials

Summarising financials

{kind=link}