In June 2026, RBL Bank got everything a struggling lender could wish for. A Gulf banking giant wrote it a cheque for Rs 26,016 crore, its credit rating jumped four notches, and its stock had already climbed about 70% from the lows of the previous year.

And yet, for FY26, it earned a Return on Assets (ROA) of just 0.55%.

A healthy private bank earns 1.5% to 2%. RBL runs at roughly a third of that.

RBL’s recovery

RBL’s recovery

So what did Emirates NBD (ENBD) actually buy? To answer that, three things are worth understanding:

1. A deliberate strategy reset since 2023 that healed one crisis without fixing another one.

2. A profitability gap that all that new capital, on its own, cannot close.

3. A valuation that has re-rated on the deal, while the operating recovery is still a work in progress.

Let’s start with how this bank got here.

Historical share price movement

Source: www,tradingview.com

Source: www,tradingview.com

Understanding the business

For roughly a decade, RBL built a high-octane engine of two unsecured businesses: credit cards and microfinance.

Under previous chief executive Vishwavir Ahuja, the bank bought Royal Bank of Scotland’s India card business in 2013, then supercharged it through a co-branded partnership with Bajaj Finance from 2016, at one point growing cards at 100% a year.

Microfinance was built in parallel, from zero branches in 2010 to a large rural book. Both are unsecured, meaning no land, property, or gold backs the loan, so they earn fat interest rates.

When times are good, they are profitable, but when times turn, they are the first to blow up. In FY25, both blew up together. The microfinance book’s Gross Non-Performing Assets (GNPA), the share of loans where borrowers have stopped paying, jumped to 17.5% by March 2025 from 4.1% a year earlier. Cards deteriorated alongside. FY25 profit collapsed 40%.

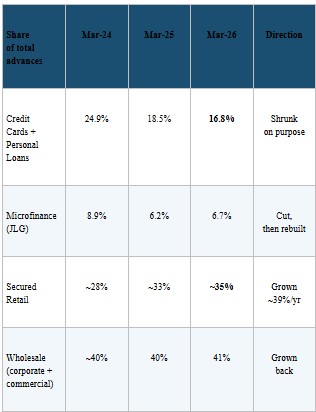

In that backdrop, R Subramaniakumar took over as the Managing Director and Chief Executive Officer in mid-2023. His answer was to rewire what kind of bank RBL was: shrink the risky, unsecured engine, and build a safer, more boring book of secured loans in its place.

Loans backed by collateral (homes, gold, business assets) earn less, but they do not detonate the way unsecured loans do.

The shift is clear in the loan mix. The share of credit cards and personal loans in total advances was cut hard, while secured retail was built almost from scratch, growing at roughly 39% a year.

Segment-wise portfolio mix change (%)

Source: CRISIL rating rationale, 22 June 2026. Mix as % of total advances

Source: CRISIL rating rationale, 22 June 2026. Mix as % of total advances

Did it work? For the two segments the strategy was meant to fix, it did, and the proof is in the segment-level bad loans.

The wholesale and secured retail books, together with most of the banks, saw their bad-loan ratios roughly halve, and then halve again.

Segment-wise gross non-performing assets (%)

Source: CRISIL rating rationale, 22 June 2026. GNPA as % of that segment’s advances

Source: CRISIL rating rationale, 22 June 2026. GNPA as % of that segment’s advances

So the reset delivered a cleaner, more diversified bank. But two things did not go to plan, and they set up everything that follows.

First, credit cards, where the clean-up is still unfinished. Second, profitability, which the very act of de-risking was meant to improve, has actually deteriorated.

Two fires: One out, one still burning

The clearest way to see which way trouble is moving in a bank is to track slippages, the fresh loans that turn bad each quarter. On that measure, RBL’s two unsecured books have gone in opposite directions.

Microfinance is a good story. Fresh slippages from the joint-liability group (JLG) book fell from Rs 472 crore in the March 2025 quarter to just Rs 87 crore a year later. The early-warning bucket of loans (borrowers just starting to miss payments) shrank dramatically, and collection efficiency climbed to 99.7%.

Better still, about 95% of the standard microfinance book is now covered by a government credit guarantee scheme, which caps the losses if a future cycle turns.

In the case of credit cards, however, slippages rose every single quarter of FY26, from Rs 479 crore to Rs 619 crore.

Slippages: Microfinance vs credit cards

Source: RBL quarterly Investor Presentations, Q4FY25 to Q4FY26. Latest quarter in bold

Source: RBL quarterly Investor Presentations, Q4FY25 to Q4FY26. Latest quarter in bold

Why are cards still bleeding? RBL brought its card collections in-house from a co-branded partner (Bajaj Finance). The CEO admitted that in pin codes where the bank lacks its own collection muscle, stress simply piled up.

Management has promised the peak is near: five separate times over five quarters, each time pushing the finish line out. The latest guidance states that elevated card slippages are a first-half FY27 problem at most, with card credit costs guidance to around 5.5% in the second half of FY27 from nearly double that of FY26.

Independent regulator data, tracked in the Thurro database, shows RBL’s cards in force did turn back up, from 4.54 million in August 2025 to 4.63 million by March 2026, so the acquisition engine has restarted. But the recovery has since stalled, flat at about 4.62 million through April and May 2026, and card spends have barely moved in over two years, around Rs 7,000 crore to 7,500 crore a month.

RBL issues more than three lakh cards a quarter just to stand still. At best, the franchise is stabilising, not growing.

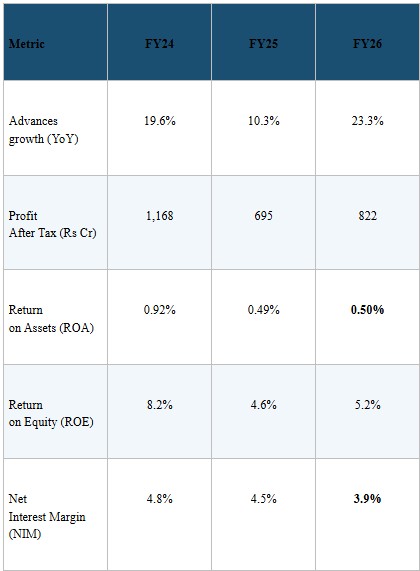

The profit puzzle: Why just 0.55%?

Here is the part that trips people up. The reset made RBL safer, and yet its profitability got worse, not better.

The table below shows that the business is growing fast and bad loans are falling, but the ROA is stuck.

Key operating indicators

Source: Motilal Oswal Limited, DuPont analysis, and ICRA rating rationale, both April to June 2026. NIM per ICRA methodology

Source: Motilal Oswal Limited, DuPont analysis, and ICRA rating rationale, both April to June 2026. NIM per ICRA methodology

The cause is the reset itself. Swapping high-yield credit cards for low-yield secured loans mechanically shrinks the margin the bank earns.

The Net Interest Margin (NIM), the gap between what the bank earns on loans and pays on deposits, fell from 4.8% to 3.9% as high-yielding cards gave way to a lower-yielding secured book. And building an in-house collections team is expensive, so operating costs stayed high at 4.4% of assets, above the roughly 3.2% average for listed private banks. A thinner margin and a fat cost base together crushed the bottom line.

The optimistic point of view is that this is the bottom. As card slippages peak and roll off, overall bank credit costs should fall toward 1.5% by the second half of FY27. Deposit costs are already easing. And the ENBD capital slashes the bank’s leverage, which flatters ROE.

Motilal Oswal Q4FY26 RBL Bank quarterly update models ROA recovery to 0.98% in FY27 and 1.34% by FY28. The bear case is even simpler: those are forecasts, and RBL has missed its own 1% exit-ROA target for FY26 already.

Emirates NBD, the second-largest bank in the United Arab Emirates, acquired roughly 60% of RBL through a fresh capital infusion of Rs 26,016 crore, one of the largest foreign investments into an Indian bank. The deal was finalised in June 2026, making RBL a subsidiary of a large international group. Importantly, this is a change of ownership, not management, because the existing team stays, and only the board composition changes.

What it changes is balance sheet strength. The bank’s core capital ratio, a cushion against losses, roughly triples from about 12.8% to around 34% on a pro-forma basis. That fortress capital drove the four-notch upgrade to AAA and gives RBL years of growth runway.

It should also lower funding costs over time. RBL today pays 5.69% for its interest-bearing funds versus 5.11% for the average private bank, a nearly 60 basis point gap from offering higher deposit rates. ICRA expects that gap to narrow: as a subsidiary of Emirates NBD, a $331 billion bank rated A1 by Moody’s, RBL should raise deposits at better rates and gain access to what the agency calls “diversified and relatively lower-cost funding sources.”

That sounds great, but what it doesn’t change is the day-to-day profitability. Capital does not fix a 0.55% ROA. Only better margins, lower costs, and lower credit losses do.

The rating agency flagged that operating costs are high, core operating profit has fallen, and a meaningful improvement in returns will take time. In other words, ENBD bought a much stronger balance sheet wrapped around an operating engine that still has to prove itself.

At about Rs 362/share, RBL is valued at roughly Rs 56,300 crore. For a bank, Price-to-Book (P/B) is a meaningful valuation measure. On that basis, RBL trades at about 1.3x times its post-deal book value.

Peer set valuation benchmarks vs ROA (%)

|

Bank |

P/B (x) |

ROA (FY26, full year) |

|

Federal Bank |

1.5x |

1.15% |

|

Yes Bank |

1.5x |

0.80% |

|

IDFC First Bank |

1.4x |

0.44% |

|

RBL Bank |

1.3x |

0.53% |

|

Bandhan Bank |

1.3x |

0.64% |

|

IndusInd Bank |

1.1x |

0.18% |

Source: Thurro database | FY26 standalone ROA as declared by each bank. P/B on the latest reported book (to early July 2026). RBL on post-ENBD book

The same picture across the wider banking sector makes the point sharper. Plot every major listed bank by ROA against P/B, and a clear upward relationship appears: banks that earn more are worth more.

RBL sits well to the right of where its 0.55% ROA would place it, priced like a bank that already earns its keep.

Bank valuation (P/B) versus profitability (ROA), FY26. Source: Thurro database

RBL is not an obvious bargain: it trades richer than IndusInd, is at the level with Bandhan, and only a little below IDFC First, yet it earns one of the thinnest ROAs in the group. At 1.3 times book, the market is already paying for a recovery that has not yet reached the profit line. The stock has re-rated on the deal and the rating.

The risks are clear. Card slippages could stay elevated longer than the promised first half of FY27. The margin recovery leans on deposit costs continuing to fall. And the bank still has an unfilled Chief Financial Officer role to close.

Specifically, what needs to be tracked is: credit-card slippages actually peaking and trending downwards in the first half of FY27, the ROA climbing from 0.55% toward the 1% the bank keeps promising, and the margin stabilising as cheaper deposits flow through.

Get those three, and a 1.3 times book multiple on an AAA-rated, well-capitalised bank starts to look cheap rather than fair.

Note: We have relied on data from http://www.Screener.in and http://www.tijorifinance.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

Rahul Rao has helped conduct financial literacy programmes for over 1,50,000 investors. He has also worked at an AIF, focusing on small and mid-cap opportunities.

Disclosure: The writer or his dependents do not hold shares in the securities/stocks/bonds discussed in the article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.

{kind=link}